Kenanga favours a few amid plastics packaging sector challenges

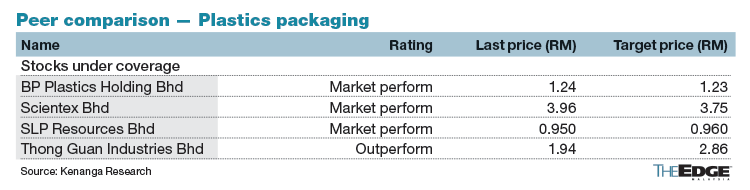

KUALA LUMPUR (Jan 30): Kenanga Research named Thong Guan Industries Bhd, SLP Resources Bhd and BP Plastics Holding Bhd (BPPlas) as the industry picks as they shift focus to high-value, high-margin products such as nano stretch film, which align well with sustainable packaging trends.

The research house likes Thong Guan as its top sector pick due to its earnings stability enhanced by a diversified product portfolio, a steadily expanding clientele base, aggressive expansion into European and US markets, and plans for premium product expansion.

Meanwhile, it said BP Plastics is favoured for its robustness in the Southeast Asia market, strong cash flows, and premium stretch film and blown film capacity expansion.

Meanwhile, Kenanga also noted the growing demand for SLP Resources Bhd’s mono film products, especially the fully recyclable MDO-PE film.

“We continue to favour SLP due to its focus on high-margin, non-commoditised products and strong financial position, enabling consistent and generous dividends,” it said in a note on Tuesday.

Additionaly, Kenanga is adjusting its projected FY24 earnings for SLP by 7% to RM16.8 million, reflecting recovering demand for its kitchen and garbage bags, as well as the anticipated increase in orders for its mono film.

Consequently, it is adjusting its SLP’s target price(TP) by 12% to 96 sen due to revisions in the FY24 dividend forecast and recalibrated WACC (weighted average cost of capital) assumptions.

Scientex Bhd is also recommended for its position as the region’s largest flexible plastic packaging manufacturer and strong demand for its affordable housing projects.

Low capacity, slow demand still

However, plastic packaging companies are finding it difficult to make the most of the subsiding resin cost because of the slow demand recovery for plastic packaging materials due to the frail global economy.

The overall industry is currently operating at about 50-60% capacity, compared to 75-80% before the pandemic.

As a result, exporters are choosing to lower their selling prices concurrently with the weaker resin cost roundabout to maintain or increase their market shares rather than increase selling prices. The current resin prices are at levels of US$1,000-1,100 (RM4,730-5,203) per tonne.

Companies are finding it challenging to pass on increases in input costs, notably from increased labour expenses and electricity tariff hikes for the industrial and commercial segments.

Kenanga noted that following the geopolitical tensions such as the Red Sea crisis, freight shipping costs have escalated.

Kenanga said the full impact of the electricity tariff hikes at the start of the year was evident after companies like BP Plastics, Scientex, and Thong Guan withdrew from the green electricity tariff (GET) programme, following the upward revision of the GET rate.

“They are now subject to the common imbalance cost pass-through (ICPT) surcharge of 17 sen/kWh. These factors collectively weigh on their profit margins,” added Kenanga.

The house said the near-term outlook for the plastic packaging market remains on the modest side, with a chance of improvement in the second half of CY24.

It cited KPMG’s forecast which predicts the global plastic packaging market to grow at a 5% CAGR from 2021 to 2026.